FHSA vs. TFSA vs. RRSP: What to Fund First in 2025 for Your First Home

FHSA vs. TFSA vs. RRSP: What to Fund First in 2025 for Your First Home

Hamed Rahimi

If you’re a first-time homebuyer in Canada in 2025, you’ve probably heard of the First Home Savings Account (FHSA), Tax-Free Savings Account (TFSA), and Registered Retirement Savings Plan (RRSP).

All three can help you save faster — but which should you prioritize if your goal is to buy a home? This guide will break down how each account works, the tax advantages, and my funding order strategy for maximum results.

Step 1: Understand the Core Purpose of Each Account

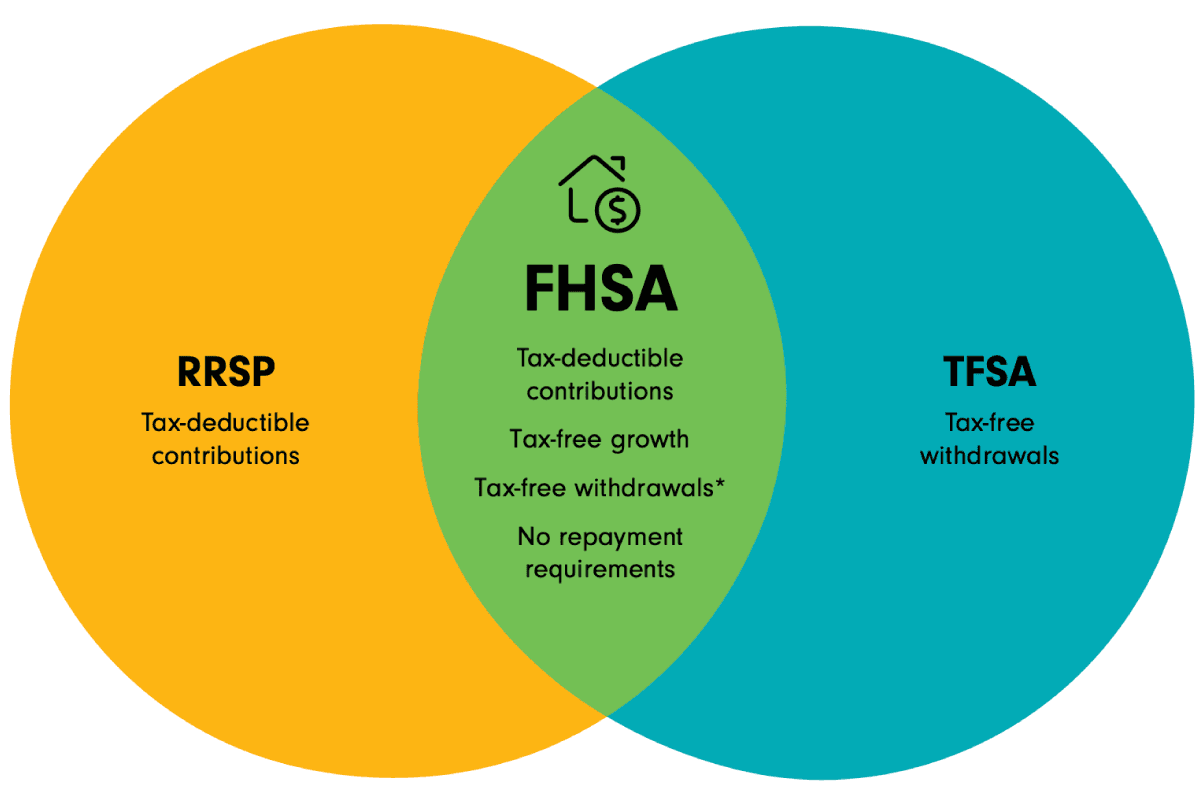

1) First Home Savings Account (FHSA)

Purpose: Save for your first home with double tax benefits — contributions are tax-deductible (like an RRSP) and withdrawals for a qualifying home are tax-free (like a TFSA).

Contribution limit: $8,000 per year (annual participation room in first year you open), $40,000 lifetime.

Best for: People planning to buy a qualifying first home within 15 years.

Extra perk: Can be combined with the Home Buyers’ Plan (HBP) to pull up to $60,000 more from RRSPs without tax at withdrawal.

📚 Read next: [The Complete FHSA Guide for 2025]

2) Tax-Free Savings Account (TFSA)

Purpose: Grow your investments tax-free — withdrawals for any reason (including a home purchase) are also tax-free.

Contribution limit (2025): $7,000 annual limit; lifetime room for someone who’s been eligible since 2009 is $95,000.

Best for: Flexible short-to-medium term savings goals — you can use TFSA funds for your home down payment, emergencies, renovations, or investing.

Extra perk: Withdrawals free up the same amount of contribution room the next calendar year.

3) Registered Retirement Savings Plan (RRSP)

Purpose: Save for retirement with an upfront tax deduction — investment growth is tax-deferred until withdrawal.

Contribution limit: 18% of previous year’s earned income, up to $32,490 for 2025, plus unused carryforward room.

Best for: Long-term retirement savings, or using the HBP to borrow up to $60,000 (per person) tax-free for a first home — repayable over 15 years.

Extra perk: If you transfer from RRSP to FHSA, you can later withdraw FHSA funds for your home with no repayment required.

Step 2: Compare the Tax Impact

Feature | FHSA | TFSA | RRSP |

|---|---|---|---|

Upfront Tax Deduction | ✅ | ❌ | ✅ |

Tax-Free Growth | ✅ | ✅ | ❌ (Tax-Deferred) |

Tax-Free Withdrawal for Home | ✅ (If Qualified) | ✅ | ❌ (unless via HBP) |

Withdrawal Repayment? | ❌ | ❌ | ✅ (HBP = 15 Years) |

Lifetime Contribution Limit | $40K | None | None (Annual Limit Only) |

Flexibility if Plans Change | Transfer to RRSP | Any Use | Keep invested until retirement |

Step 3: The Funding Order I Recommend for Most First-Time Buyers (2025)

1️⃣ FHSA First

You only get 15 years from opening to use it.

Double tax advantage makes it unbeatable for a first home goal.

Even if you’re unsure about buying soon, open it now to start building participation room.

2️⃣ TFSA Second

Flexible — you can still use it for your home, or keep it for other goals.

Great place for emergency savings while you’re building your down payment.

No penalty or repayment if you decide not to buy.

3️⃣ RRSP Third (for HBP)

Use if you want to stack FHSA + HBP for a larger down payment.

Transfer from RRSP to FHSA if you want tax-free home withdrawals without HBP repayment.

Step 4: Smart Combinations for Maximum Impact

Scenario A: Couple Buying in 3–5 Years

Each person maxes FHSA ($8K/year) → $64K combined in 4 years.

Both use TFSA to top up flexible savings.

Optionally add RRSP contributions to leverage HBP ($60K each).

Scenario B: Solo Buyer with High Income

Max FHSA for deduction in top bracket.

Put surplus into RRSP for another deduction and HBP potential.

Keep TFSA for flexibility and as a rate-shock buffer.

Scenario C: Unsure About Buying

Still open FHSA to start the clock.

Fund TFSA until purchase plans solidify.

Transfer FHSA to RRSP if you decide not to buy.

Step 5: Avoid These Mistakes

❌ Waiting to open an FHSA — you lose valuable participation room.

❌ Using TFSA for speculative, high-risk investments if you need the funds soon.

❌ Forgetting HBP repayments — missing them turns them into taxable income.

❌ Over-contributing to any account — CRA penalties are 1% per month.

Final Word

If your primary goal is to buy a home, the FHSA is the clear #1 choice in 2025. From there, fill your TFSA for flexibility, and then RRSP if you want to leverage the HBP or transfer funds to FHSA.

The key is timing your contributions for maximum tax impact while keeping your savings accessible when you find the right property.

💡 Want to know exactly how much to put in each account based on your income and purchase timeline?

I run these calculations for clients every day — saving thousands in taxes and years off their savings goal.

If you’re a first-time homebuyer in Canada in 2025, you’ve probably heard of the First Home Savings Account (FHSA), Tax-Free Savings Account (TFSA), and Registered Retirement Savings Plan (RRSP).

All three can help you save faster — but which should you prioritize if your goal is to buy a home? This guide will break down how each account works, the tax advantages, and my funding order strategy for maximum results.

Step 1: Understand the Core Purpose of Each Account

1) First Home Savings Account (FHSA)

Purpose: Save for your first home with double tax benefits — contributions are tax-deductible (like an RRSP) and withdrawals for a qualifying home are tax-free (like a TFSA).

Contribution limit: $8,000 per year (annual participation room in first year you open), $40,000 lifetime.

Best for: People planning to buy a qualifying first home within 15 years.

Extra perk: Can be combined with the Home Buyers’ Plan (HBP) to pull up to $60,000 more from RRSPs without tax at withdrawal.

📚 Read next: [The Complete FHSA Guide for 2025]

2) Tax-Free Savings Account (TFSA)

Purpose: Grow your investments tax-free — withdrawals for any reason (including a home purchase) are also tax-free.

Contribution limit (2025): $7,000 annual limit; lifetime room for someone who’s been eligible since 2009 is $95,000.

Best for: Flexible short-to-medium term savings goals — you can use TFSA funds for your home down payment, emergencies, renovations, or investing.

Extra perk: Withdrawals free up the same amount of contribution room the next calendar year.

3) Registered Retirement Savings Plan (RRSP)

Purpose: Save for retirement with an upfront tax deduction — investment growth is tax-deferred until withdrawal.

Contribution limit: 18% of previous year’s earned income, up to $32,490 for 2025, plus unused carryforward room.

Best for: Long-term retirement savings, or using the HBP to borrow up to $60,000 (per person) tax-free for a first home — repayable over 15 years.

Extra perk: If you transfer from RRSP to FHSA, you can later withdraw FHSA funds for your home with no repayment required.

Step 2: Compare the Tax Impact

Feature | FHSA | TFSA | RRSP |

|---|---|---|---|

Upfront Tax Deduction | ✅ | ❌ | ✅ |

Tax-Free Growth | ✅ | ✅ | ❌ (Tax-Deferred) |

Tax-Free Withdrawal for Home | ✅ (If Qualified) | ✅ | ❌ (unless via HBP) |

Withdrawal Repayment? | ❌ | ❌ | ✅ (HBP = 15 Years) |

Lifetime Contribution Limit | $40K | None | None (Annual Limit Only) |

Flexibility if Plans Change | Transfer to RRSP | Any Use | Keep invested until retirement |

Step 3: The Funding Order I Recommend for Most First-Time Buyers (2025)

1️⃣ FHSA First

You only get 15 years from opening to use it.

Double tax advantage makes it unbeatable for a first home goal.

Even if you’re unsure about buying soon, open it now to start building participation room.

2️⃣ TFSA Second

Flexible — you can still use it for your home, or keep it for other goals.

Great place for emergency savings while you’re building your down payment.

No penalty or repayment if you decide not to buy.

3️⃣ RRSP Third (for HBP)

Use if you want to stack FHSA + HBP for a larger down payment.

Transfer from RRSP to FHSA if you want tax-free home withdrawals without HBP repayment.

Step 4: Smart Combinations for Maximum Impact

Scenario A: Couple Buying in 3–5 Years

Each person maxes FHSA ($8K/year) → $64K combined in 4 years.

Both use TFSA to top up flexible savings.

Optionally add RRSP contributions to leverage HBP ($60K each).

Scenario B: Solo Buyer with High Income

Max FHSA for deduction in top bracket.

Put surplus into RRSP for another deduction and HBP potential.

Keep TFSA for flexibility and as a rate-shock buffer.

Scenario C: Unsure About Buying

Still open FHSA to start the clock.

Fund TFSA until purchase plans solidify.

Transfer FHSA to RRSP if you decide not to buy.

Step 5: Avoid These Mistakes

❌ Waiting to open an FHSA — you lose valuable participation room.

❌ Using TFSA for speculative, high-risk investments if you need the funds soon.

❌ Forgetting HBP repayments — missing them turns them into taxable income.

❌ Over-contributing to any account — CRA penalties are 1% per month.

Final Word

If your primary goal is to buy a home, the FHSA is the clear #1 choice in 2025. From there, fill your TFSA for flexibility, and then RRSP if you want to leverage the HBP or transfer funds to FHSA.

The key is timing your contributions for maximum tax impact while keeping your savings accessible when you find the right property.

💡 Want to know exactly how much to put in each account based on your income and purchase timeline?

I run these calculations for clients every day — saving thousands in taxes and years off their savings goal.

If you’re a first-time homebuyer in Canada in 2025, you’ve probably heard of the First Home Savings Account (FHSA), Tax-Free Savings Account (TFSA), and Registered Retirement Savings Plan (RRSP).

All three can help you save faster — but which should you prioritize if your goal is to buy a home? This guide will break down how each account works, the tax advantages, and my funding order strategy for maximum results.

Step 1: Understand the Core Purpose of Each Account

1) First Home Savings Account (FHSA)

Purpose: Save for your first home with double tax benefits — contributions are tax-deductible (like an RRSP) and withdrawals for a qualifying home are tax-free (like a TFSA).

Contribution limit: $8,000 per year (annual participation room in first year you open), $40,000 lifetime.

Best for: People planning to buy a qualifying first home within 15 years.

Extra perk: Can be combined with the Home Buyers’ Plan (HBP) to pull up to $60,000 more from RRSPs without tax at withdrawal.

📚 Read next: [The Complete FHSA Guide for 2025]

2) Tax-Free Savings Account (TFSA)

Purpose: Grow your investments tax-free — withdrawals for any reason (including a home purchase) are also tax-free.

Contribution limit (2025): $7,000 annual limit; lifetime room for someone who’s been eligible since 2009 is $95,000.

Best for: Flexible short-to-medium term savings goals — you can use TFSA funds for your home down payment, emergencies, renovations, or investing.

Extra perk: Withdrawals free up the same amount of contribution room the next calendar year.

3) Registered Retirement Savings Plan (RRSP)

Purpose: Save for retirement with an upfront tax deduction — investment growth is tax-deferred until withdrawal.

Contribution limit: 18% of previous year’s earned income, up to $32,490 for 2025, plus unused carryforward room.

Best for: Long-term retirement savings, or using the HBP to borrow up to $60,000 (per person) tax-free for a first home — repayable over 15 years.

Extra perk: If you transfer from RRSP to FHSA, you can later withdraw FHSA funds for your home with no repayment required.

Step 2: Compare the Tax Impact

Feature | FHSA | TFSA | RRSP |

|---|---|---|---|

Upfront Tax Deduction | ✅ | ❌ | ✅ |

Tax-Free Growth | ✅ | ✅ | ❌ (Tax-Deferred) |

Tax-Free Withdrawal for Home | ✅ (If Qualified) | ✅ | ❌ (unless via HBP) |

Withdrawal Repayment? | ❌ | ❌ | ✅ (HBP = 15 Years) |

Lifetime Contribution Limit | $40K | None | None (Annual Limit Only) |

Flexibility if Plans Change | Transfer to RRSP | Any Use | Keep invested until retirement |

Step 3: The Funding Order I Recommend for Most First-Time Buyers (2025)

1️⃣ FHSA First

You only get 15 years from opening to use it.

Double tax advantage makes it unbeatable for a first home goal.

Even if you’re unsure about buying soon, open it now to start building participation room.

2️⃣ TFSA Second

Flexible — you can still use it for your home, or keep it for other goals.

Great place for emergency savings while you’re building your down payment.

No penalty or repayment if you decide not to buy.

3️⃣ RRSP Third (for HBP)

Use if you want to stack FHSA + HBP for a larger down payment.

Transfer from RRSP to FHSA if you want tax-free home withdrawals without HBP repayment.

Step 4: Smart Combinations for Maximum Impact

Scenario A: Couple Buying in 3–5 Years

Each person maxes FHSA ($8K/year) → $64K combined in 4 years.

Both use TFSA to top up flexible savings.

Optionally add RRSP contributions to leverage HBP ($60K each).

Scenario B: Solo Buyer with High Income

Max FHSA for deduction in top bracket.

Put surplus into RRSP for another deduction and HBP potential.

Keep TFSA for flexibility and as a rate-shock buffer.

Scenario C: Unsure About Buying

Still open FHSA to start the clock.

Fund TFSA until purchase plans solidify.

Transfer FHSA to RRSP if you decide not to buy.

Step 5: Avoid These Mistakes

❌ Waiting to open an FHSA — you lose valuable participation room.

❌ Using TFSA for speculative, high-risk investments if you need the funds soon.

❌ Forgetting HBP repayments — missing them turns them into taxable income.

❌ Over-contributing to any account — CRA penalties are 1% per month.

Final Word

If your primary goal is to buy a home, the FHSA is the clear #1 choice in 2025. From there, fill your TFSA for flexibility, and then RRSP if you want to leverage the HBP or transfer funds to FHSA.

The key is timing your contributions for maximum tax impact while keeping your savings accessible when you find the right property.

💡 Want to know exactly how much to put in each account based on your income and purchase timeline?

I run these calculations for clients every day — saving thousands in taxes and years off their savings goal.

Get my latest mortgage tips, tools, and guides — delivered right to you.

No spam, unsubscribe anytime.